.png) 8 hours ago

1

8 hours ago

1

By any measure, Africa’s digital economy is expanding at speed, but the cost of staying connected still varies sharply across its largest markets.

From Lagos to Cairo and Johannesburg to Nairobi, the price of mobile data, voice calls, and SMS is shaping not just consumer behaviour, but the pace of innovation, financial inclusion, and digital trade.

A Continent of Contrasts

The accusation that telecom operators in Africa charge expensive tariffs is common, but the data tells a more nuanced story. Prices may feel high to consumers, yet in many cases, operators are not the primary drivers of those costs.

Let’s unpack it:

Across Africa’s top 10 economies, typically including Nigeria, South Africa, Egypt, Algeria, Kenya, Morocco, Ethiopia, Ghana, Angola, and Tanzania, the disparity in telecom pricing reflects deeper structural realities: infrastructure gaps, regulatory policies, currency volatility, and competition levels.

Mobile data, now the backbone of digital access, shows the widest variation. Nigeria, Ghana, and Kenya consistently rank among the cheapest markets, with average costs for 1GB as low as $0.37, $0.40, and $0.59 respectively.

In contrast, South Africa, despite its advanced telecom infrastructure, records significantly higher prices, averaging around $1.77 per GB.

Egypt and Morocco sit somewhere in the middle, benefiting from relatively mature markets and regulatory interventions that have kept prices competitive.

Nigeria’s Paradox: Cheap Data, Rising Pressure

Nigeria, one of Africa’s largest economies, presents a paradox. On one hand, it boasts some of the lowest data prices globally, around $0.38 per GB, driven largely by intense competition among operators and a large subscriber base.

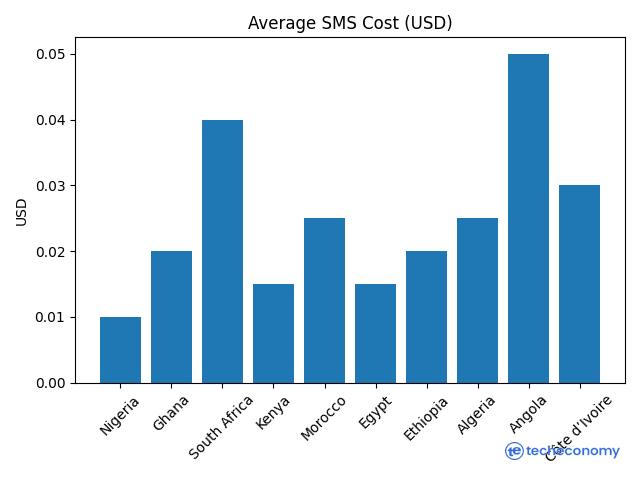

On the other hand, recent tariff adjustments highlight underlying strain. In 2025, regulators approved increases in voice and SMS rates, pushing call costs to roughly ₦15.40 per minute and SMS to about ₦5.60.

This reflects a broader industry challenge: while data may be cheap, maintaining network quality amid inflation, currency depreciation, and energy costs is becoming increasingly difficult.

Voice and SMS: Declining but Still Critical

While global trends show a shift away from traditional voice and SMS toward data-driven messaging apps, these services remain vital across Africa, especially in rural and low-income segments.

Yet, Africans still pay disproportionately high rates for voice services relative to income. Studies indicate that mobile users on the continent spend significantly more on voice packages as a share of earnings than users in other regions.

In many top economies, voice and SMS pricing is influenced by regulatory floors, taxation, and limited competition.

Countries like Ethiopia and Angola, where telecom markets are less liberalized, tend to have higher and less flexible pricing structures compared to Nigeria or Kenya.

Why the Gaps Persist

Several factors explain the pricing divide among Africa’s biggest economies:

1. Infrastructure Deficits – Higher Cost per GB

Across Africa, over 80% of internet users rely onmobile broadband, not fixed fibre. This matters because fibre cost per GB is significantly lower than mobile data, and tower-based networks require diesel, maintenance, and backhaul, raising costs. For instance,

- Nigeria: Fibre penetration estimated at <15% of population

- Kenya: ~20–25% fibre reach, boosted by urban rollout

- South Africa: highest fibre-to-home penetration among major African markets

The result is that countries with limited fibre like Nigeria depend heavily on mobile networks, pushing operators’ costs, and ultimately prices higher.

2. Market Competition Drives Prices Down

There’s a strong inverse relationship between number of active operators and data prices.

Comparative structure:

- Nigeria: 4 major operators – MTN, Airtel, Glo, T2 – but the marketing it tilting towards duopoly (see here).

- Kenya: 3-4 active players, but strong competition led by Safaricom vs Airtel

- South Africa: More concentrated, with MTN and Vodacom dominating ~70%+ market share

- Egypt: Smaller competitive spread, with strong state influence

The pricing outcome is that economies like Nigeria & Kenya are often among the lowest data prices in Africa, as low as $0.30–$1 per GB in some bundles, primarily due to price wars, bundle innovation, and cheaper consumer data while places like South Africa and Egypt are historically higher prices, though declining after regulatory pressure.

3. Regulation & Taxes Add Invisible Costs

Telecom pricing is heavily shaped by government policy. Some African countries impose sector-specific taxes up to 30–40% on telecom services; spectrum licensing fees can run into hundreds of millions of dollars, and import duties on telecom equipment increase capex.

From Techeconomy analysis, these countries present somewhat contradictory environments. For instance, Nigeria faces multiple taxes coupled with right-of-way charges across states; Kenya has a more streamlined regulatory environment, though still taxed; and South Africa has high spectrum costs, which have historically slowed expansion..

The truth is that operators pass these costs to consumers, meaning higher taxes = higher data prices.

4. Currency Volatility Inflates Telecom Costs

Telecom is a dollarized industry. Equipment for base stations, fibre cables (now more fibre companies are springing up in Nigeria), routers, amongst others, are imported. In some markets, the operators source dollar from the parallel market.

It may interest you to know that international bandwidth is priced in USD! The impact of currency depreciation as felt in Nigeria is such that naira lost over 60% of its value between 2023 and 202; Egypt faced multiple devaluations which increased telecom costs, and Kenya witnessed more stability, but still pressured.

When these happen, operators’ costs rise sharply in local currency, price increases are delayed due to regulation/competition, and eventually, tariffs adjust upward or quality drops.

These dynamics mean that even where nominal prices appear low, affordability, measured against income, can still be a challenge.

The Bigger Picture: Affordability vs Accessibility

Despite progress, Sub-Saharan Africa is challenged by expensive mobile data relative to income, reinforcing a persistent digital divide.

For policymakers, the challenge is no longer just about lowering prices, but about ensuring sustainable pricing models that encourage investment while expanding access.

A Race Against Time

As artificial intelligence, fintech, and digital services reshape global economies, the cost of connectivity will increasingly determine Africa’s competitiveness.

The top 10 economies are not just competing on GDP, they are competing on who can connect their populations faster, cheaper, and more reliably.

In that race, affordability is only half the story. The real test is whether low prices can translate into meaningful access, and ultimately, into economic transformation.

The post How Africa’s Top 10 Economies Compare on Data, Voice & SMS Tariffs appeared first on Tech | Business | Economy.